[ad_1]

Most readers would already bear in mind that Kendrion’s (AMS:KENDR) inventory elevated considerably by 12% over the previous three months. Nonetheless, on this article, we determined to concentrate on its weak fundamentals, as long-term monetary efficiency of a enterprise is what finally dictates market outcomes. Particularly, we determined to check Kendrion’s ROE on this article.

Return on Fairness or ROE is a check of how successfully an organization is rising its worth and managing buyers’ cash. Briefly, ROE reveals the revenue every greenback generates with respect to its shareholder investments.

View our latest analysis for Kendrion

How To Calculate Return On Fairness?

The method for ROE is:

Return on Fairness = Web Revenue (from persevering with operations) ÷ Shareholders’ Fairness

So, primarily based on the above method, the ROE for Kendrion is:

5.8% = €9.9m ÷ €172m (Based mostly on the trailing twelve months to December 2023).

The ‘return’ is the yearly revenue. One other method to think about that’s that for each €1 value of fairness, the corporate was in a position to earn €0.06 in revenue.

What Is The Relationship Between ROE And Earnings Development?

So far, we have now discovered that ROE measures how effectively an organization is producing its earnings. Relying on how a lot of those earnings the corporate reinvests or “retains”, and the way successfully it does so, we’re then in a position to assess an organization’s earnings progress potential. Assuming all else is equal, corporations which have each a better return on fairness and better revenue retention are normally those which have a better progress price when in comparison with corporations that do not have the identical options.

Kendrion’s Earnings Development And 5.8% ROE

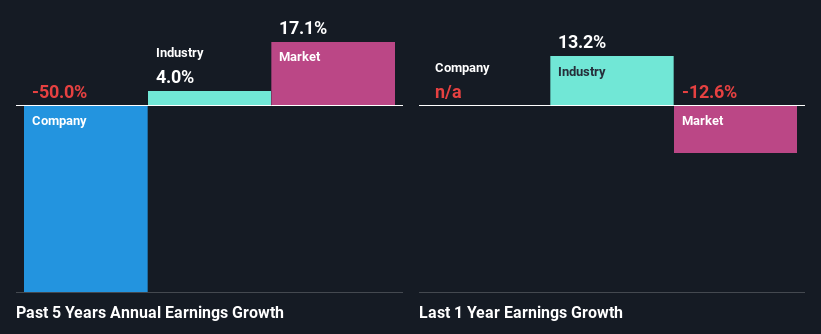

At first look, Kendrion’s ROE would not look very promising. Subsequent, when in comparison with the common business ROE of 8.7%, the corporate’s ROE leaves us feeling even much less enthusiastic. Given the circumstances, the numerous decline in web revenue by 50% seen by Kendrion during the last 5 years isn’t a surprise. We reckon that there may be different components at play right here. For instance, it’s attainable that the enterprise has allotted capital poorly or that the corporate has a really excessive payout ratio.

That being stated, we in contrast Kendrion’s efficiency with the business and had been involved once we discovered that whereas the corporate has shrunk its earnings, the business has grown its earnings at a price of 4.0% in the identical 5-year interval.

Earnings progress is a big think about inventory valuation. What buyers want to find out subsequent is that if the anticipated earnings progress, or the dearth of it, is already constructed into the share value. This then helps them decide if the inventory is positioned for a vibrant or bleak future. Is Kendrion pretty valued in comparison with different corporations? These 3 valuation measures may aid you determine.

Is Kendrion Making Environment friendly Use Of Its Earnings?

Kendrion’s declining earnings isn’t a surprise given how the corporate is spending most of its earnings in paying dividends, judging by its three-year median payout ratio of 73% (or a retention ratio of 27%). With solely little or no left to reinvest into the enterprise, progress in earnings is way from doubtless. To know the two dangers we have now recognized for Kendrion go to our risks dashboard for free.

Moreover, Kendrion has paid dividends over a interval of a minimum of ten years, which signifies that the corporate’s administration is decided to pay dividends even when it means little to no earnings progress. Upon finding out the most recent analysts’ consensus information, we discovered that the corporate’s future payout ratio is anticipated to drop to 41% over the subsequent three years. The truth that the corporate’s ROE is anticipated to rise to 11% over the identical interval is defined by the drop within the payout ratio.

Conclusion

General, we might be extraordinarily cautious earlier than making any determination on Kendrion. As a result of the corporate is just not reinvesting a lot into the enterprise, and given the low ROE, it is not shocking to see the dearth or absence of progress in its earnings. With that stated, we studied the most recent analyst forecasts and located that whereas the corporate has shrunk its earnings previously, analysts count on its earnings to develop sooner or later. To know extra in regards to the firm’s future earnings progress forecasts check out this free report on analyst forecasts for the company to find out more.

Have suggestions on this text? Involved in regards to the content material? Get in touch with us straight. Alternatively, e-mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is basic in nature. We offer commentary primarily based on historic information and analyst forecasts solely utilizing an unbiased methodology and our articles aren’t meant to be monetary recommendation. It doesn’t represent a advice to purchase or promote any inventory, and doesn’t take account of your goals, or your monetary state of affairs. We intention to carry you long-term targeted evaluation pushed by elementary information. Observe that our evaluation could not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link